Why Do Property Investors Network At Live Events In Norwich, But Don't Learn How To Get Started With Little Or No Money Down?

Are you a beginner to property investing, looking to attend your first network meeting, have little of no money to get started, and need advice on what to say and do? Let's get you ready with some of the right questions to ask!

What's Happening In The Norwich Market Today

The Norwich property market remains relatively stable, supported by the city’s strong local economy, two universities, and its role as the commercial and cultural centre of Norfolk. While price growth has moderated in line with national trends, demand for both owner-occupied and rental property remains consistent. Norwich is often seen as more affordable than many southern cities, but affordability pressures are still present, particularly for first-time buyers and leveraged investors.

Some things to expect:

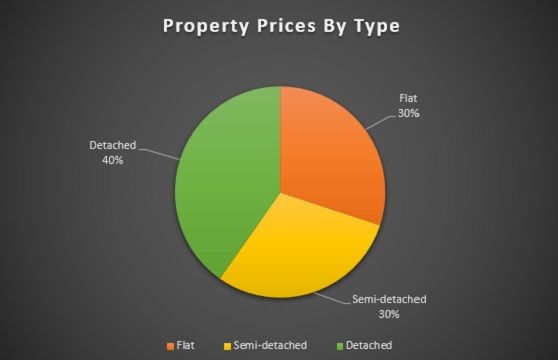

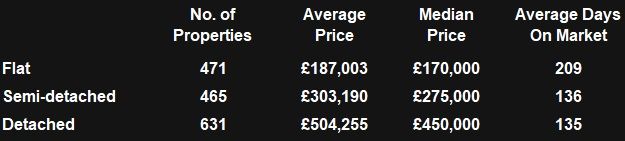

Competition for properties: According to the accompanying graphs and data, 70% of house sales come from semi-detached and terraced houses and tend to sell more quickly than flats (30%), reflecting sustained demand from families and long-term renters. These property types benefit from broader buyer appeal and better resale liquidity. Flats, while still common—particularly in and around the city centre—generally remain on the market for longer periods, suggesting more cautious buyer sentiment, often linked to service charges, lease terms, and yield considerations. Well-located houses in popular residential areas continue to attract competitive interest when priced realistically.

Upfront costs are still significant: This is the case, even though prices in Norwich are lower than in many larger UK cities. With greater scope for multiple variations of strategies, and the greater abundance of houses compared to flats, let's use a house with a market value on a semi-detached house of £300,000 as our case example. Therefore, with a 15% discount (£45,000) on a £300,000 property (purchase price £255,000), the upfront cash deposit, Stamp Duty Land Tax (SDLT) and fees will be approximately £79,250 (see summary below).

Additional challenges for non-local investors: Rental demand, tenant profiles, and capital growth prospects can differ markedly between the city centre, inner suburbs, and surrounding villages. Investors unfamiliar with Norwich may underestimate the impact of conservation areas, older housing stock, and local planning considerations, all of which can increase costs or restrict development options. Understanding which areas attract students, professionals, or families is critical to aligning strategy with demand.

Tenant management: This is generally stable, but still requires active oversight. The rental market is driven by a mix of students from the University of East Anglia and Norwich University of the Arts, healthcare workers, public-sector employees, and families. While this diversity can provide resilience, it also means landlords must manage differing expectations around property standards and tenancy length. Rising regulatory requirements, energy-efficiency standards, and local enforcement activity increase the administrative burden, particularly for landlords managing properties remotely.

Summary

Market Value: £300,000

Less Discount: £45,000

Purchase Price: £255,000

Cost of Savings:

£63,750 (Your Savings / Existing Equity) + £15,500 (Stamp Duty Land Tax)

Total Cost: £79,250 *

* While yields can be strong, the initial outlay remains a hurdle for many.

That is why your few minutes on this page can expand your vision. With that in mind, start searching Google for "property investor meetings Norwich".

During the networking sessions, ask this one key question: “How can you realistically get started with little or no money?” You may even get a 20-second speaking opportunity to ask the room to approach you during the break with their advice.

Most likely you will hear of some doing deal sourcing — finding properties for others in exchange for a commission. That is one way, but you are acting more like a middleman, in some ways like an estate agent, but for a higher percentage commission.

Something else you may hear will be to active joint-venture partner with someone you know who is the money partner in the arrangement. You do the work, and your funder is the silent partner, just approving the go-ahead and supplying the funding. You split profits 50%-50%.

There are alternative methods that don’t require large savings, and some of them were once popular across the UK after the 2008 financial crisis — and still work today. My colleague and I have adapted and taught these approaches for over 20 years, and we’ve put them together in a free multimedia resource. It explores practical ways to start investing with minimal upfront cash. While you don’t need to study it before attending an event, knowing these approaches will help you ask better questions and see the bigger picture.

Once likely entry costs are understood, the next step is selecting an approach that aligns with Norwich’s market profile. Flats are generally best suited to standard Buy-to-Let strategies aimed at students or young professionals, though longer selling periods and service charges should be factored into exit planning. Houses, particularly terraced and semi-detached properties in areas such as Hellesdon, Sprowston, and Costessey, lend themselves well to long-term family rentals or light refurbishment-led investments rather than intensive HMO strategies. With increasing regulatory requirements, energy-efficiency standards, and compliance obligations, careful planning is especially important for non-local investors seeking stable, lower-turnover returns.

Where people describe often mention creative models like "purchase lease options", they mostly remain tied to traditional borrowing — bridging loans, mortgages, or investor funding. In other words, even “creative” strategies generally assume you already have access to cash or credit. We popularised options in the UK around the time of the 2008 Global Financial Crisis, yet subsequently these strategies have been watered-down in property training circles to be used with mainstream lending.

Obviously, not every seller is motivated, and not every property will result in a deal. Even in a market like Norwich, many deals fall down due to the buyer or seller changing their mind, or a dependent chain breaking down. This is we we prefer property without a dependent forward purchase involved.

For beginners without significant savings — perhaps juggling a full-time job or unsure where to start — this can feel discouraging. Many newcomers attend a meeting once, realise the upfront barriers, and don’t return. Others invest heavily in mentorship programmes (£10K–£25K per year) hoping for shortcuts, only to discover the fundamentals still require capital and credit.

Over 25 years of developing and teaching property strategies in the UK, I’ve seen cycles repeat. When lending tightens — as it is today — investors face higher deposits, stricter criteria, and increased regulation. Yet, these conditions also highlight opportunities that many overlook.

Understanding these points will help you attend your first Norwich networking event with realistic expectations and better preparation. Opportunities haven’t vanished — they’ve simply shifted. Some of the most effective strategies are still accessible with minimal upfront investment. One approach allows investors to start with virtually no capital and very little competition:

✅ No mortgage required

✅ No mortgage applications

✅ No savings, home equity, or borrowings needed

✅ No stamp duty payable

This method was widely used across the UK post-2008 and remains effective today. When shared at meetings, attendees often nod politely and return to conventional, more expensive strategies.

If you’re dedicating time to learn and network, it’s worth exploring alternatives that reduce both financial and learning barriers. This strategy is detailed in a free multimedia series, featuring videos, audio, and PDF chapters derived from a former #1 real estate book, “How to Control a House for a $1 Deposit and No Mortgage Needed.”

It’s designed for those who want to understand property control and creative deal structures from home — even if you’re short on capital or just starting your property journey in Norwich.

Other Locations