Up until now, we’ve seen how most property investors focus on a narrow slice of a massive market — chasing deals that demand significant time, money, and effort to convert into high-yielding income properties.

To make the numbers work, they buy large houses or commercial buildings, split them into smaller units, apply for multiple rounds of council approvals, and battle through layers of regulation. Then come the maintenance costs, tenant disputes, and the constant wear-and-tear that quietly eats away at profit. By contrast, I vividly recall one investor at a property meeting lamenting in frustration that all his profits for the year had been completely wiped out by emergency repair costs on his rental property. He was a visibly stressed buy-to-let landlord.

Many investors tell me it can take months just to get an offer accepted for the first property — because competition for these properties is fierce. Yet most presenters at live events skip over these real-world challenges. They highlight the success stories, but gloss over the costly mistakes made along the way.

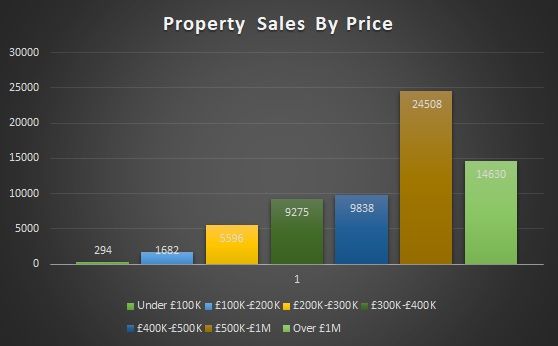

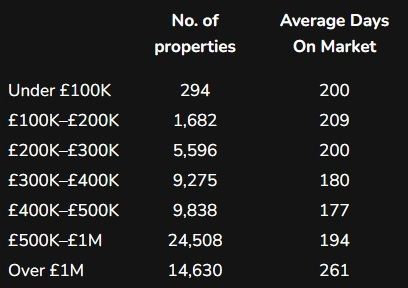

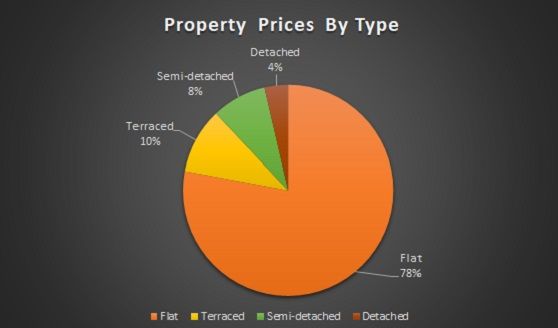

But the market data tells a different story. Properties are taking longer to sell, which means motivated sellers are everywhere. The real opportunity isn’t in fighting over the same limited stock — it’s in stepping outside the crowd to spot deals others overlook, across all categories of property (as shown in the charts).

Over the past year, I attended more than forty investor networking events across London. Again and again, I saw the same pattern: people nod along, agree that London isn’t viable for buy-to-let, then either spend thousands on “education” programs or give up entirely — still stuck in their 9-to-5 financial rut.

But the real opportunity is hiding in plain sight.

A strategy that lets you invest with virtually no competition:

✅ No mortgage required

✅ No mortgage applications

✅ No savings, home equity, or borrowings needed

✅ No stamp duty payable

It was once one of the UK’s most powerful post-crisis approaches — and it still works today.

Yet when I share it, people smile and say, “Interesting…” and then go and do the exact opposite! If you are going to put in the time and effort to attend your local property network meeting, at least be forearmed with an alternative approach that has minimal upfront costs and learning curve compared to what's popular and more complex to learn.

Click on the button below for videos and 23 chapters in audio and PDF format taken from a previous #1 best seller in real estate books, "How to Control a House for a $1 Deposit and No Mortgage Needed".