What's Happening In The Leeds Market Today

Leeds attracts investors from across the UK, especially

from the more expensive south of England. Prices here are generally lower,

which can make investing more accessible.

Some things to expect:

Competition

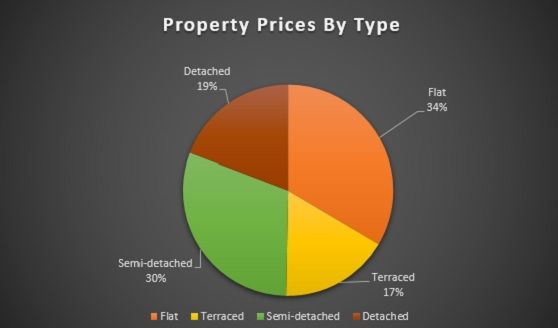

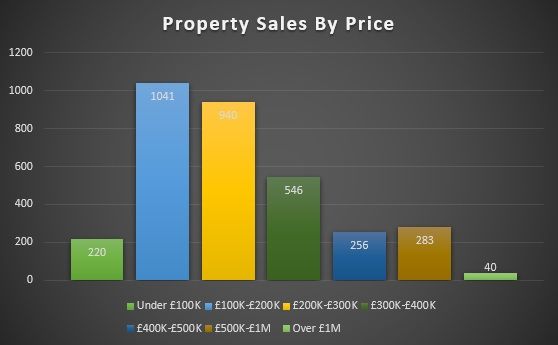

for properties: As per the above chart and data, the most

active price range is typically £100,000–£300,000, and these homes

tend to sell faster than in southern markets — refer to the above chart and data.

Upfront

costs are still significant: Even with a 15% discount

(£30,000) on a £200,000 property (purchase price £170,000), the upfront

cash deposit, Stamp Duty Land Tax (SDLT) and fees will be over £50,000 (see

summary below).

Additional

challenges for non-local investors: You’ll need to arrange

builders, gas and electrical engineers, and letting agents if you don’t

live locally. Without a local presence, you may be spending more than what

others do who are familiar with the market.

Tenant

management: Shared accommodations or Houses in

Multiple Occupation (HMOs) can create more “people problems”,

particularly if you’re managing from a distance.

Summary

Market Value: £200,000

Less Discount: £30,000

Purchase Price: £170,000

Cost of Savings:

£42,500 (Your Savings / Existing Equity) + £9,400 (Stamp Duty Land Tax)

Total Cost: £51,900

Even seasoned investors encounter these challenges. For beginners without substantial savings, it’s easy to leave property investor meetings feeling discouraged. Many attendees only come once, mentally confirming what they suspected about the costs and hurdles involved.

Despite the above advanced warnings, you should attend a property investors’ network meeting in your Leeds area to confirm for yourself what are your options. Typing the following into Google, “property investor meetings leeds”, will show you venues nearby. When you attend, consider asking experienced investors this one key question: “How can you realistically get started with little or no money?” The most common answer you will hear is to be a deal sourcer (introducer) working on commission, but that is not a strategy.

However, alternative strategies do exist that were popularised in the UK after the 2008 Global Financial Crisis — and still work today. They are explained in a free multimedia resource that my colleague and I have developed and used over the last 20 years. It explores ways to start property investment with minimal upfront cash. While this isn’t required to attend an event, understanding these approaches can give you context and help you see the bigger picture.