Why Do Property Investors Network At Live Events In Liverpool, But Don't Learn How To Get Started With Little Or No Money Down?

Do you have little savings to get started with most property investing strategies? Attend your first property meeting and know the right questions to ask!

What's Happening In The Liverpool Market Today

The Liverpool property market remains one of the most active and investor-focused in the UK, underpinned by a large rental population, multiple universities, major employers, and ongoing regeneration. While market conditions have cooled compared with the post-pandemic peak, transaction levels and rental demand remain robust, particularly at the more affordable end of the market (£100,000 - £300,000). Liverpool continues to attract both owner-occupiers and investors seeking lower entry prices than those found in southern cities.

Some things to expect:

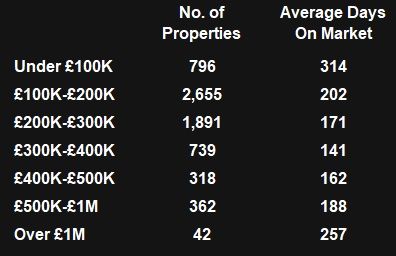

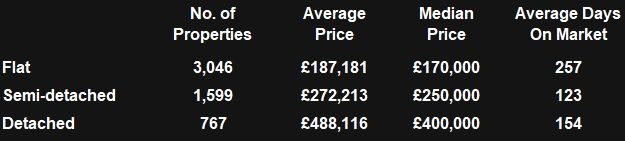

Competition for properties: This varies significantly by property type and price band. Flats make up the largest share of available stock, but they also record the longest average time on market (around 250+ days), reflecting oversupply in certain city-centre developments and buyer caution around service charges. In contrast, semi-detached houses, which form a substantial portion of listings, sell more quickly on average (around four months), driven by family demand and stronger owner-occupier appeal. Well-priced houses in popular suburbs often attract strong competition, particularly from landlords targeting long-term rentals or HMOs.

Upfront costs are still significant: Even though Liverpool is often considered an affordable city, average flat prices sit below £200,000, but stamp duty, mortgage costs, furnishing, and potential remediation work in older blocks can materially increase total investment costs. For houses, average prices rise sharply by type, with detached properties averaging well above £450,000, placing them firmly outside entry-level investor budgets. Rising interest rates have also reduced leverage and placed greater emphasis on cash flow and yield resilience. Using £250,000 as an example sale price, a 15% discount (£37,500) would make for a £212,500 purchase price, with the upfront cash deposit, Stamp Duty Land Tax (SDLT) and fees approximately £65,500 (see summary below).

Additional challenges for non-local investors: Liverpool’s market is highly fragmented, with large differences between postcodes, neighbourhoods, and even streets. Certain areas benefit from strong tenant demand and regeneration investment, while others suffer from oversupply or weaker resale prospects. Understanding licensing requirements, Article 4 directions in selected wards, and local tenant expectations requires on-the-ground knowledge. Investors unfamiliar with Liverpool may also underestimate management intensity in high-turnover student or shared accommodation stock.

Tenant management: The city supports students, young professionals, families, and benefit-supported tenants, each with different management demands. While yields can be attractive, particularly in shared housing, higher turnover, maintenance, and compliance obligations are common. Increasing regulation, energy-efficiency standards, and selective licensing schemes mean that active management — or the use of competent local agents — is essential, especially for landlords operating remotely.

Summary

Market Value: £250,000

Less Discount: £37,500

Purchase Price: £212,500

Cost of Savings:

£53,125 (Your Savings / Existing Equity) + £12,375 (Stamp Duty Land Tax)

Total Cost: £65,500 *

* While yields can be strong, the initial outlay remains a hurdle for many.

With strategies like BRRR, Commercial-to-Residential conversions, Rent2Rent, HMOs, etc being spoken about, do some of your own research in advance for asking informed questions and understanding the local market context. You can find venues nearby by searching "property investor meetings Liverpool" on Google.

When you go, ask this one key question: “How can you realistically get started with little or no money?” You’ll likely hear that the only option is deal sourcing — finding properties for others in exchange for a commission. But that’s not a long-term investment strategy. Some may suggest to find a (silent) money partner and you be the (active) partner on a profit-share basis.

There are alternative methods that don’t require large savings, and some of them were once popular across the UK after the 2008 financial crisis — and still work today. My colleague and I have adapted and taught these approaches for over 20 years, and we’ve put them together in a free multimedia resource. It explores practical ways to start investing with minimal upfront cash. While you don’t need to study it before attending an event, knowing these approaches will help you ask better questions and see the bigger picture.

As with any investment strategy, understanding local geography, demographics, and planning policy is essential. Liverpool City Council operates selective licensing schemes in several wards, including parts of Kensington, Picton, and Wavertree, and has implemented Article 4 directions affecting new HMOs in high-density student areas. Market conditions can vary sharply between neighbourhoods such as the Baltic Triangle, L7, L6, and south Liverpool suburbs like Aigburth or Mossley Hill. Reviewing live listings on Rightmove or Zoopla by postcode is critical to assessing achievable rents and resale demand, and investors should always consult the council’s planning and private-rented-sector guidance before pursuing HMO or conversion strategies.

Once likely entry costs are understood, the next step is selecting an approach that aligns with Liverpool’s market profile. Flats often suit standard Buy-to-Let or student-focused rental strategies in the city centre and Baltic Triangle, though service charges and longer selling periods require careful consideration. Houses may support Buy-Refurbish-Rent, HMO (where permitted), or long-term family rentals depending on location, with areas such as Wavertree and Old Swan remaining popular for shared housing. With increasing regulation, licensing requirements, and energy-efficiency standards, careful planning is particularly important for non-local investors managing higher-turnover assets.

All of the above chart and data does not tell the full story, as not every property transaction converts into a profitable strategy. Even in a busy market like Liverpool, many deals fall through once financing, refurbishment, or resale timelines are factored in.

For beginners without significant savings — perhaps juggling a full-time job or unsure where to start — this can feel discouraging. Many newcomers attend a meeting once, realise the upfront barriers, and don’t return. Others invest heavily in mentorship programmes (£10K–£25K per year) hoping for shortcuts, only to discover the fundamentals still require capital and credit.

Over 25 years of developing and teaching property strategies in the UK, I’ve seen cycles repeat. When lending tightens — as it is today — investors face higher deposits, stricter criteria, and increased regulation. Yet, these conditions also highlight opportunities that many overlook.

Understanding these points will help you attend your first Birmingham networking event with realistic expectations and better preparation. Opportunities haven’t vanished — they’ve simply shifted. Some of the most effective strategies are still accessible with minimal upfront investment. One approach allows investors to start with virtually no capital and very little competition:

✅ No mortgage required

✅ No mortgage applications

✅ No savings, home equity, or borrowings needed

✅ No stamp duty payable

This method was widely used across the UK post-2008 and remains effective today. When shared at meetings, attendees often nod politely and return to conventional, more expensive strategies.

If you’re dedicating time to learn and network, it’s worth exploring alternatives that reduce both financial and learning barriers. This strategy is detailed in a free multimedia series, featuring videos, audio, and PDF chapters derived from a former #1 real estate book, “How to Control a House for a $1 Deposit and No Mortgage Needed.”

It’s designed for those who want to understand property control and creative deal structures from home — even if you’re short on capital or just starting your property journey in Liverpool.

Other Locations