1. Seller Scenario

[COPY]+[PASTE] The Text Below Into A New ChatGPT Thread

Please model the following contract of sale into two

separate parts: one for the property owner and one for the creative investor.

A property owner purchased a house in November 2020 for

£575,000 using a £57,500 deposit and a capital-and-interest mortgage of

£517,500 at 3%, with a fixed monthly payment of £2,454.04. This amount remains intact and unchanged for the duration of the agreement.

After 52 months (March 2025), the outstanding mortgage

balance is £453,153.07.

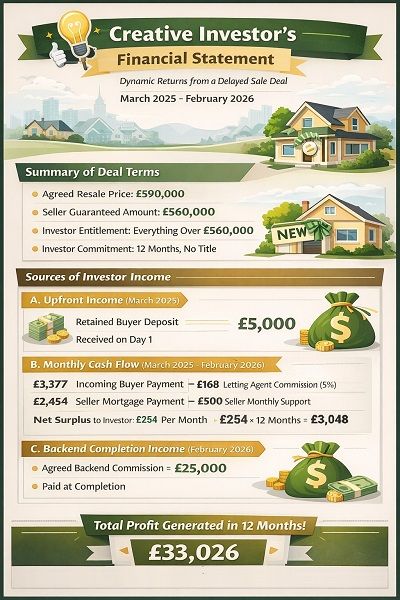

In March 2025, the owner agrees to a delayed sale

arrangement with a creative investor and an end buyer. The owner agrees to

receive £560,000 out of the transaction, and the creative investor receives

anything above the amount with the end buyer.

The creative investor markets that house for £590,000 with

an end buyer providing purchase deposit of £40,000, leaving an upfront balance

of £550,000.

At the start of the arrangement: From that £40,000

deposit, £35,000 is paid to the seller upfront (used to clear £19,632 of mortgage arrears, £10,000 in unsecured debts and the balance £5,368 cash towards relocation expenses). The investor receives the balance of £5,000 upfront

from the buyer’s deposit.

During the 12-month period (March 2025 – February 2026):

– The seller receives £500 per month for 12 months (£6,000

total).

– The investor hires a managing agent to receive the fixed

monthly instalment of £3,377.48 for a capital-and-interest schedule of £550,000 at

5.5%.

Monthly payment schedule, paid via the managing agent:

Buyer monthly payment: £3,377.48

Less: £2,454.04 seller's monthly instalment

£500 capital payment to owner

£168.87 agent's commission (5%)

£254.57 creative investor (independent monthly income)

– At final completion (February 2026):

– £25,000 of the sale

price is paid to the investor as the backend margin for his management of the

sale.

– The seller’s mortgage is redeemed at £437,079.32.

At the time of completion 12 months later, the transaction

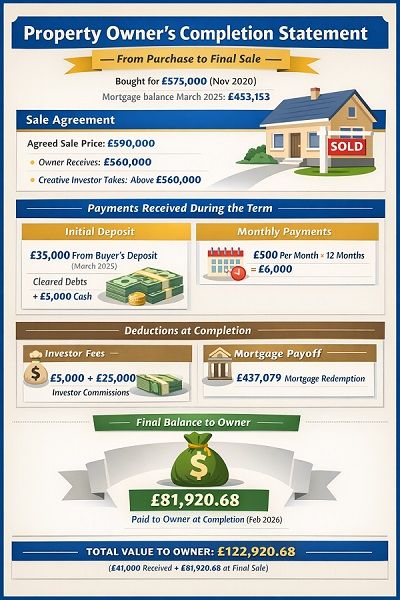

for the owner is as follows, according to the breakdown of payments received:

Sale price: £590,000

Less: £35,000

deposit received (March 2025)

£5,000

investor part-paid commission (March 2025)

£6,000 12 x

£500 monthly payments (March 2025 – February 2026)

£25,000

investor balance-paid commission (February 2026)

£437,079.32

mortgage redemption due (February 2026)

£81,920.68

balance to owner before legal fees (February 2026)

Please produce an owner-focused completion statement that reconciles

the money flow during the overall transaction. The output should be clear,

educational, and suitable for novice investors to follow.

2. Creative Investor Scenario

[COPY]+[PASTE] The Text Below Into The Same ChatGPT Thread

Can you now create a financial statement on behalf of the creative investor from the above data?